Here's your preview of this week's big market-moving events

REUTERS/Jacky NaegelenStock market operator Euronext's analysts work in the market services surveillance room at the new Euronext headquarters in Courbevoie near Paris, France, November 12, 2015.

At least 129 people were killedafter terrorists orchestrated a series of attacks in Paris on Friday.

Many more were critically injured.

But the world goes on.

Here's your Monday Scouting Report:

Top Stories

- How the markets react to terrible tragedies. Experts expect a knee-jerk reaction to Friday's events when markets open on Monday. While it feels a bit awkward and callous to discuss this so soon, the timing of this discussion matters if it can offer guidance to those on the brink of dumping the risk in their portfolios. (Note: French financial markets will open as usual on Monday.)

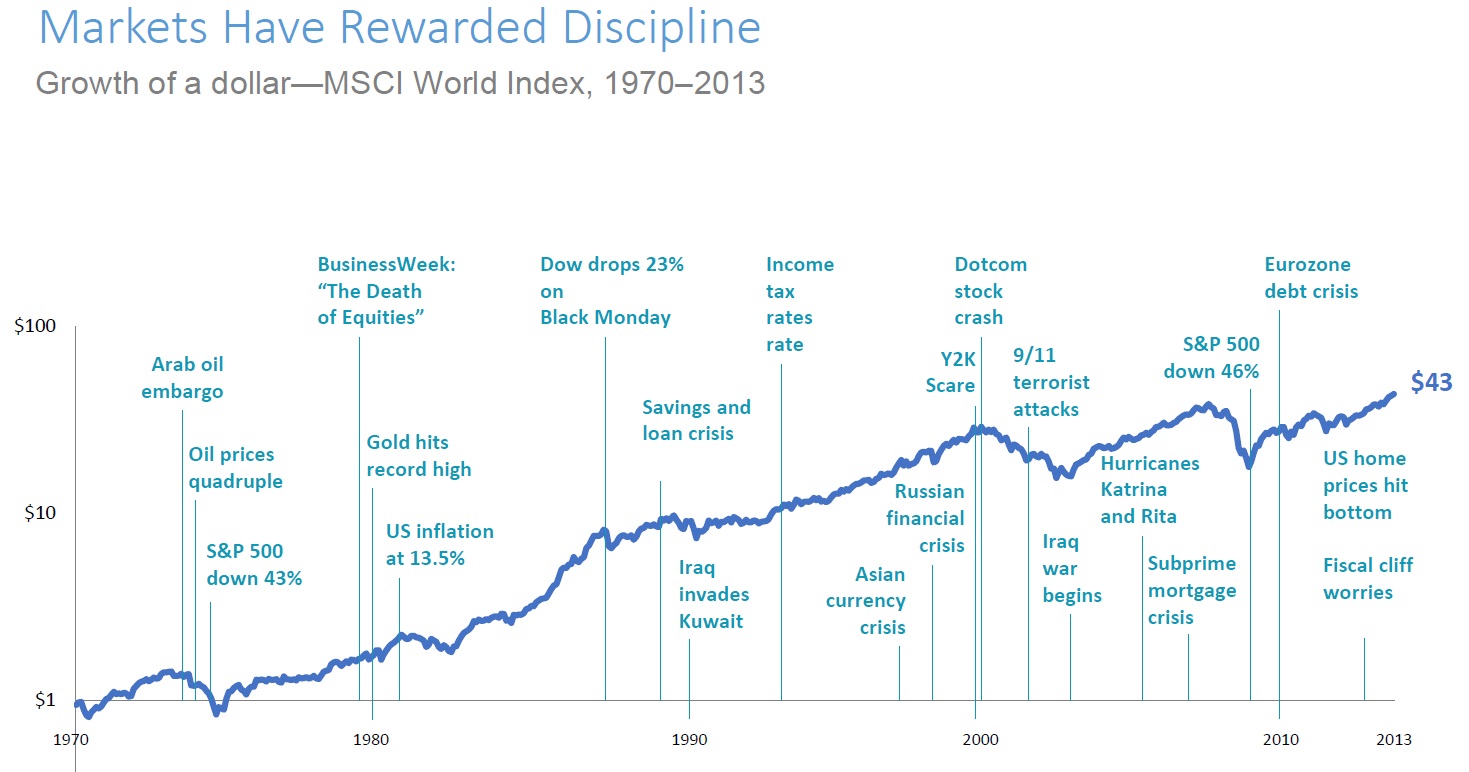

Sadly, there is no shortage of horrible events in history. Ritholtz Wealth Management's Josh Brown reviews some of the worst ones that occurred in the past century and notes that stocks often end flat to higher within days or just a few months. Crossing Wall Street's Eddy Elfenbein went into this in depth two years ago. Warren Buffett wrote about it in the New York Times seven years ago.

So what's this about? Brean Capital's Peter Tchir offered a thoughtful take on Sunday: "In spite of many doomy predictions surrounding past events, the resilience of the people has won out over terror. People have not given up in the past. People do not huddle up cowering in their homes. They get out and go about their business and defy the people who perpetrated such acts. If the security forces can do their job I would not bet against the people. If there is not another attack in the immediate aftermath, then I would expect the people to once again manage to overcome the attack. Human nature is full of struggle against oppression and will hopefully prevail again." - A warning from retail. On Friday, we learned retail sales in October were a bit weaker than expected. (For what it's worth, the September and August reports also whiffed.) “[I]t is very risky to use retail sales as a proxy for real consumption - which is what really matters,” said Pantheon Macroeconomics’ Ian Shepherdson, who argues the real story is being held back by the weak inflation story.

But there could be something more significant happening here with the American consumer, who has been one of the most bullish forces in the global economy. Here'swhat analysts said after department store giant Nordstrom reported a horrible third quarter: "With a superior business model, in our view, that is half high-end dept. store, 30% off-price, and 20% online, this level of deceleration is a potential cautionary tale of the US consumer's health," Deutsche Bank said. "We think we are either seeing the impact of one of the warmest fall selling seasons in recent history (more likely) or we are teetering on the precipice of a recession,” KeyBanc said.

REUTERS/Kacper PempelPeople stand in line to sign a condolence book in memory of the victims of the attacks in Paris, at the French embassy in Warsaw, Poland November 15, 2015.

Economic Calendar

- Empire Manufacturing (Mon): Economists estimate this regional manufacturing index improved to -6.35 in November from -11.36 in October. Here's Deutsche Bank's Joe LaVorgna: "The New York Fed Empire survey is expected to remain in negative territory for the fourth consecutive month and for the fifth time in the last six months. On an ISM-adjusted basis, the headline Empire series stood at 46.3 last month, which tells us the economy could be in an industrial recession. Within the Empire data, pay close attention to the new orders, employment and shipments figures—both new orders and shipments are below the headline number, pointing to further downward momentum in the latter. The six-month outlook is also worth paying attention to—it stood at 23.4 in October, up slightly from September’s 23.2 reading, which was the lowest level since January 2013 (22.7)."

- Consumer Price Index (Tues): Economists estimate consumer prices climbed by 0.2% month-over-month in October or 0.1% year-over-year. Excluding food and energy, core prices are estimated to have increased by 0.2% and 1.9%, respectively. Here's Wells Fargo's Sam Bullard: "Consumer price inflation has remained soft, with the headline index weighed down by energy and import prices. After falling 9% in September, gasoline prices should exert a substantially smaller drag in October. Core CPI continues to be supported by shelter costs and medical care, a trend which should continue. While headline inflation should remain subdued for the next couple of months, low base effects should begin to work into the yearoveryear calculation–staring in Q1 2016–and result in a sharply higher inflation performance than we have seen in 2015."

- Industrial Production (Tues): Economists estimate production increased by 0.1% in October as capacity utilization stood at 77.5%. Here's Nomura: "Regional manufacturing surveys were mostly weak again in October; however, the ISM manufacturing survey, which provides a measure of national manufacturing sentiment, declined only slightly on the month and the Chicago PMI surprised to the upside. In addition, the Bureau of Labor Statistics (BLS) reported that aggregate hours worked in manufacturing rose in October. As such, we expect an increase in manufacturing production in October. Based on the BLS aggregate hours worked in mining, we forecast that mining production was roughly unchanged. We also expect little change in vehicle production again in October. Weekly utility output data point to a decline in utilities production in October, possibly due to a warmer-than-usual October and thus less heating demand."

- NAHB Housing Market Index (Tues): Economists estimate this index of homebuilder sentiment was unchanged at 64 in November. Here's Bank of America Merrill Lynch: "After reaching a cyclical high of 64 in October, we think the risk is that homebuilder sentiment edges down to a 62 reading. This is still indicative of a robust housing market. However, we think builders have become increasingly frustrated by the lack of labor and inability to increase supply, as discussed in the housing watch."

- Housing Starts (Wed): Economists estimate the pace of starts dropped 3.8% to 1.160 million units in October. Building permits climbed 3.9% to 1.149 million units. Here's Nomura: "The broad improvement in housing starts this year suggests that improving household fundamentals, favorable demographics, and low mortgage interest rates are finally feeding through to the housing market. Multifamily starts increased at a very strong pace in most regions in September – indicative of household formations occurring increasingly in the rental space as people transition to renting before homeownership due to financial constraints – but we expect to see some payback in this metric in October as the multifamily series tends to be volatile … We are constructive on housing activity in the medium term, largely based on: 1) pent-up demand from a depressed pace of household formation; and 2) improvement in the employment and income outlook for younger workers."

- FOMC Minutes (Wed): The Fed will release the minutes of its Oct. 27-28 Federal Open Market Committee meeting at 2:00 p.m. ET. Here's RBC's Tom Porcelli: "The Fed went out of its way to make the October FOMC statement much more hawkish than expected. Beyond this, a handful of committee members (including Yellen and Dudley) have come out since then to echo that sentiment. So it would be a surprise if the Minutes did not reflect a committee that is poised to hike in December barring a negative headline in the next few weeks. Remember, the meeting took place before we received a very strong October payroll report. So the minutes are somewhat stale and we would imagine sentiment amongst the FOMC is even marginally more hawkish now than just a few weeks ago. Surely the mid-200K NFP print will help the committee to pitch a December rate hike (our base case) even more convincingly. On the heels of a stellar October payroll report, a rate increase at the December meeting seems as close to a lock as one is going to get—at this juncture."

- Initial Jobless Claims (Thurs): Economists estimate initial claims slipped to 270,000 from 276,000.

- Philadelphia Fed Business Outlook (Thurs): Economists estimate this regional activity index improved to -0.8 in November from -4.5. Here's HSBC: "Growth in US manufacturing activity has slowed noticeably this year. Slower global industrial output growth, downward pressure on international commodity prices, and an appreciation of the USD have each created challenges for export-oriented manufacturers."

- Kansas City Fed Manufacturing (Fri): Economists estimate this regional activity index improved to 0 in November from -1.

Fedspeak Calendar. From Wells Fargo's Sam Bullard: "Another bountiful week of Fed official speaking engagements awaits the financial markets. On Tuesday, Federal Reserve Governor Powell (voter, moderate) speaks in New York on “Central Clearing in an Independent World.” Later in the day, Former Fed Chairman Bernanke and Fed Governor Tarullo (voter, dove) speak at the Brookings Institution on “Are we safer? A look at the financial system, postcrisis.” Wednesday proves to be a busy day with the October 2728 FOMC meeting minutes release and four Fed speakers–New York Fed President Dudley (voter, dove), Atlanta Fed President Lockhart (voter, moderate) and Cleveland Fed President’s Mester (voter, hawk) speak on a panel in New York to The Clearing House’s annual conference; separately, Dallas Fed President Kaplan (nonvoter) speaks in Houston on “A Discussion of Economic Conditions and Federal Reserve Policy.” On Thursday, Atlanta Fed President Lockhart speaks in Atlanta on the U.S. economy; followed by Fed Vice Chairman Fischer (voter, moderate) speaking at a San Francisco Fed conference on a speech titled “Emerging Asia in Transition.” On Friday, St. Louis Fed President Bullard (2016 voter, hawk) speaks in Arkansas on the U.S. economy. On Saturday, San Francisco Fed President Williams (voter, dove) speaks in Berkeley on U.S. monetary policy. The financial markets will continue to gather clues as to individual and voting FOMC member leanings heading into the final monetary policy meeting of the year."

REUTERS/Lucas JacksonTraders work on the floor of the New York Stock Exchange shortly after an announcement by the Federal Reserve Bank in New York, October 28, 2015.

Market Commentary

As 2015 nears its close, more and more Wall Street strategists are looking to 2016.

Credit Suisse global equity strategist Andrew Garthwaite on Thursday: "We see five major headwinds for equities: Equity valuations are close to fair value … Macro uncertainty and abnormal bottom-up risk … Earnings momentum is weak … The political landscape is becoming less corporate-friendly … Market breadth falling.” “Why we remain constructive on equities: Bull markets seldom peak at fair value … Equities are still pricing in a considerable fall in economic momentum … Excess liquidity is supportive … Corporate sector net buying is set to remain high … A fall in earnings is needed for an equity bear market … First Fed rate hikes do not mark the end of a bull market." Garthwaite reiterated his firm's mid-2016 S&P 500 target of 2,200.

Barclays head of equity strategist Ian Scott on Thursday: "With the US interest rate cycle likely to turn in December, our most robust conclusion is a market driven more by considerations of value than quality or growth. In terms of sectors, we think the market shift to a focus on value favors Financials, some late-cycle cyclicals such as Materials, Industrials and Energy. On the other hand, Staples and Healthcare, as well as Utilities and Telecom, could struggle globally. Regionally, this suggests “international” equities over the US." Scott sees the S&P 500 ending 2016 at 2,200.

{kind=link}

{kind=link}